Arconic Board Affirms: Company has Right Leadership, Right Strategy to Deliver Shareholder Value

March 24, 2017

Elliott Management’s Analysis of Arconic Fundamentally Flawed, Misleading

Urges Shareholders to Protect their Investment and Vote the WHITE Proxy Card

The Independent Directors of Arconic (NYSE: ARNC) Board mailed a letter to shareholders today in connection with its upcoming Annual Meeting of Shareholders to be held on May 16, 2017. Additional information is available at www.arconic.com/annualmeeting.

The full text of the letter follows:

Protect The Value of Your Investment:

VOTE THE WHITE PROXY CARD TODAY “FOR” THE RIGHT BOARD, THE RIGHT LEADERSHIP TEAM AND THE RIGHT STRATEGY

March 24, 2017

Dear Fellow Arconic Shareholder,

At Arconic’s Annual Meeting of Shareholders on May 16, 2017, you will be asked to make an important decision that will significantly impact the future of the Company and the value of your investment. We write to you as independent directors of Arconic to urge you to keep Arconic strong by voting “FOR” Arconic’s five director nominees and Arconic’s governance proposals on the WHITE proxy card.

Arconic’s Board is Independent and Dedicated to Serving Shareholders’ Best Interests

The Arconic Board of Directors has 12 independent directors–seven who have joined the Board within the last 14 months and five who have served longer. We are committed to the interests of all Arconic shareholders.

It is our duty to oversee the Company’s strategic plan, evaluate management and ensure we have the right leadership in place to create value.

We bring to this task diverse backgrounds: many of us have been CEO's of large and complex organizations in the same industries that Arconic serves, others have served on boards of directors of similarly complex companies, and still others have had successful careers in the investment and financial services sector. For all of us, nothing is more important than ensuring Arconic is on the best path to create value for our shareholders and ensuring we have the right leadership team in place.

Arconic’s Management Team has a Proven Track Record of Success

Arconic was launched just five months ago, after the multi-year transformation of Alcoa Inc. was completed and Arconic’s business was separated from Alcoa Corporation.

Under the leadership of Klaus Kleinfeld, Alcoa Inc. was significantly transformed. The commodity businesses that became Alcoa Corporation were restructured to ensure competitiveness; high cost plants were closed, new pricing mechanisms were introduced and the businesses were strongly positioned to operate self-sufficiently. At the same time, Arconic’s world class portfolio of assets was carefully built. Management invested in innovation and enhanced manufacturing capabilities, entered growth markets and exited lower margin businesses. Overall, the management team strengthened Alcoa Inc.’s balance sheet and improved the Company’s cost structure. The executive team delivered these results for shareholders, while strengthening customer relationships, delivering a world class employee safety record, further increasing employee engagement and lowering greenhouse gas emissions.

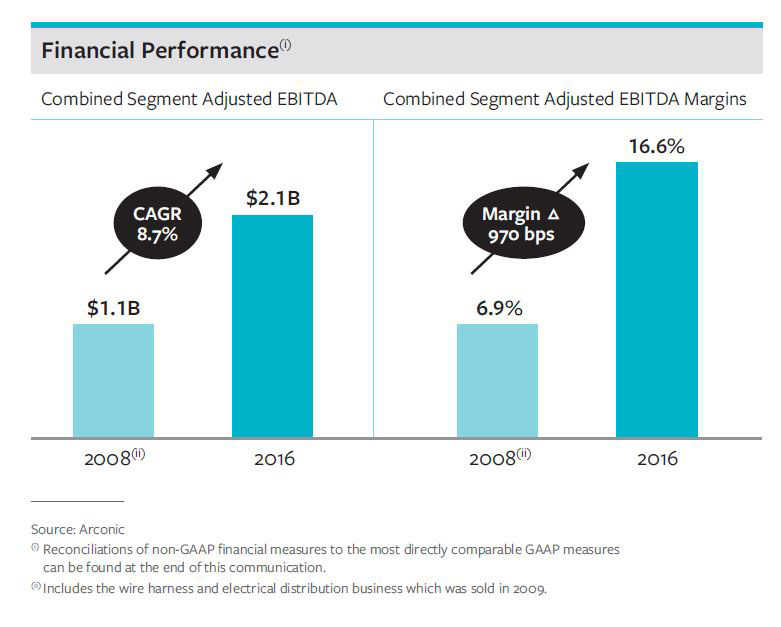

As proof of management’s success, over the last eight years, earnings1 in the Arconic businesses grew at more than 8% per year and profitability2 more than doubled. Today, nearly 80% of our revenues come from business lines in which we are the market leader or second in the market.

Perhaps even more significantly, following the successful transformation of Alcoa Inc., Mr. Kleinfeld and his team recognized that the two portfolios they had created were more valuable as separate companies. With the support of the Board, Mr. Kleinfeld led a complex and highly successful separation that created Alcoa Corporation and Arconic as two, strong, standalone public companies. Since the separation, Arconic has delivered total shareholder return (TSR) of 57%3, and we are on track to deliver sustained shareholder value over the long term.

To break up a 128-year old company like Alcoa Inc. is a significant undertaking. The success of the separation and the value it has created for shareholders show that Mr. Kleinfeld both understands what it takes to create value and has the execution capabilities to get the job done.

Arconic’s management team's execution record has earned the confidence of the Board. We are convinced that we have the right strategy and the right team to deliver shareholder value both today and over the long term.

Arconic’s Independent Directors Carefully Reviewed Elliott Management’s Analysis and Determined that it is Flawed

As you may know, one of Arconic’s shareholders, a hedge fund named Elliott Management, is seeking to place four people of its choosing onto the Board and replace the Company’s CEO, Mr. Kleinfeld. We listen eagerly and openly to the views of Arconic’s shareholders. And, indeed, we have listened carefully to Elliott: in fact, we have held nine meetings with Elliott’s representatives since 2015.

Over the past 14 months your Board added seven new directors, including three directors originally recommended by Elliott. As directors of the Company, we have unique access to internal information and a front-row seat to the execution of the Company’s business plan. We have visited operating facilities, spoken with many employees, heard from customers and suppliers and reviewed countless pages of internal documents and analyses.

Our conclusion is clear: Arconic has the Right Strategy and the Right Team to Drive Short-Term and Long-Term Value for Shareholders

The Board has made its determination about strategy and leadership after carefully considering the views of Elliott, other shareholders and outside advisors.

Our extensive review of Elliott’s claims has made it clear to us that their campaign has been largely focused on criticizing and attacking, with few details regarding any actual alternative plan, and that they have a fundamentally flawed view of what is needed to maximize Arconic’s value on a sustainable basis. Their claims do not provide a full or accurate picture of either the past or future prospects of the Company under current management, and should be viewed with skepticism. For example, Elliott:

- Compares Arconic to companies that are materially different;

- Misuses and misunderstands industry data; and

- Fails to fully appreciate that close, collaborative partnerships with our key customers are a critical ingredient for our future success.

We believe that Elliott’s criticisms are grounded in analytical work that is not accurate and does not reflect the complexity of Arconic’s markets or the skillfulness of management’s execution.

The Board Recommends Shareholders Keep Arconic on a Strong Path and Vote “FOR” Arconic’s Nominees and Governance Proposals

Arconic has laid out a clear path to create value for shareholders; we have a three-year plan to:

- Grow revenue 7-8%4 per year

- Increase profitability by expanding margins from 16.6% to ~19%5

- Reduce debt by $1 billion in 2017

- Double our Free Cash Flow from ~$350 million in 2017 to ~$700 million in 2019

- Optimize Return on Net Assets from 7.1% to 11-12% through operating performance and focus on capital efficiency

This is a plan that will deliver shareholder value, and your Board is committed to holding management accountable for delivering that value.

We are asking you to consider that a board of 12 independent directors is better positioned to determine the direction and leadership of Arconic than a hedge fund.

We have had extensive engagement with Elliott; we have heard their views and implemented changes where we thought their suggestions made sense. We believe we would be doing our shareholders a grave disservice if we substituted Elliott’s judgment for our own.

Your Board unanimously recommends that shareholders vote FOR Arconic’s five highly qualified candidates – Amy E. Alving, David P. Hess, Klaus Kleinfeld, Ulrich “Rick” Schmidt and Ratan N. Tata – which is a vote in favor of the Company’s strategic plan and a Board that is committed to creating value for all shareholders.

KEEP ARCONIC ON A STRONG PATH. PLEASE VOTE THE WHITE PROXY CARD TODAY.

Thank you for your continued support.

| The Independent Directors of Arconic Inc.: | ||||

| Patricia F. Russo, Lead Independent Director | Amy E. Alving | |||

| Arthur D. Collins, Jr. | Rajiv L. Gupta | |||

| David P. Hess | Sean O. Mahoney | |||

| E. Stanley O’Neal | John C. Plant | |||

| L. Rafael Reif | Julie G. Richardson | |||

| Ulrich R. Schmidt | Ratan N. Tata |

|

Your Vote Is Important, No Matter How Many or How Few Shares You Own |

|

Please vote today by telephone, via the Internet or by signing, dating and returning the enclosed WHITE proxy card. Simply follow the easy instructions on the WHITE proxy card. |

| If you have questions or need assistance, please contact: |

| INNISFREE M&A INCORPORATED |

| Shareholders Call Toll-Free: (877) 750-5836 |

| Banks and Brokers Call Collect: (212) 750-5833 |

|

REMEMBER: |

|

Please simply discard any Blue proxy card that you may receive from Elliott Management. |

|

Submitting a proxy using a Blue proxy card – even if you “withhold” on Elliott Management’s nominees – will revoke any vote you had previously submitted on Arconic’s WHITE proxy card. |

About Arconic

Arconic (NYSE: ARNC) creates breakthrough products that shape industries. Working in close partnership with our customers, we solve complex engineering challenges to transform the way we fly, drive, build and power. Through the ingenuity of our people and cutting-edge advanced manufacturing techniques, we deliver these products at a quality and efficiency that ensure customer success and shareholder value. For more information: www.arconic.com. Follow @arconic: Twitter, Instagram, Facebook, LinkedIn and YouTube.

Dissemination of Company Information

Arconic intends to make future announcements regarding Company developments and financial performance through its website at www.arconic.com.

Forward–Looking Statements

This communication contains statements that relate to future events and expectations and as such constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include those containing such words as “anticipates,” “believes,” “could,” “estimates,” “expects,” “forecasts,” “guidance,” “goal,” “intends,” “may,” “outlook,” “plans,” “projects,” “seeks,” “sees,” “should,” “targets,” “will,” “would,” or other words of similar meaning. All statements that reflect Arconic’s expectations, assumptions or projections about the future, other than statements of historical fact, are forward-looking statements, including, without limitation, forecasts relating to the growth of end markets and potential share gains; statements and guidance regarding future financial results or operating performance; and statements about Arconic’s strategies, outlook, business and financial prospects. Forward-looking statements are not guarantees of future performance, and it is possible that actual results may differ materially from those indicated by these forward-looking statements due to a variety of risks and uncertainties, including, but not limited to: (a) deterioration in global economic and financial market conditions generally; (b) unfavorable changes in the markets served by Arconic; (c) the inability to achieve the level of revenue growth, cash generation, cost savings, improvement in profitability and margins, fiscal discipline, or strengthening of competitiveness and operations anticipated from restructuring programs and productivity improvement, cash sustainability, technology advancements, and other initiatives; (d) changes in discount rates or investment returns on pension assets; (e) Arconic’s inability to realize expected benefits, in each case as planned and by targeted completion dates, from acquisitions, divestitures, facility closures, curtailments, expansions, or joint ventures; (f) the impact of cyber attacks and potential information technology or data security breaches; (g) political, economic, and regulatory risks in the countries in which Arconic operates or sells products; (h) the outcome of contingencies, including legal proceedings, government or regulatory investigations, and environmental remediation; and (i) the other risk factors discussed in Arconic’s Form 10-K for the year ended December 31, 2016, and other reports filed with the U.S. Securities and Exchange Commission (SEC). Arconic disclaims any obligation to update publicly any forward-looking statements, whether in response to new information, future events or otherwise, except as required by applicable law. Market projections are subject to the risks discussed above and other risks in the market.

Non-GAAP Financial Measures

Some of the information included in this communication is derived from Arconic’s consolidated financial information but is not presented in Arconic’s financial statements prepared in accordance with accounting principles generally accepted in the United States of America (GAAP). Certain of these data are considered “non-GAAP financial measures” under SEC rules. These non-GAAP financial measures supplement our GAAP disclosures and should not be considered an alternative to the GAAP measure. Reconciliations to the most directly comparable GAAP financial measures and management’s rationale for the use of the non-GAAP financial measures can be found below. Arconic has not provided a reconciliation of any forward-looking non-GAAP financial measures to the most directly comparable GAAP financial measures because Arconic is unable to quantify certain amounts that would be required to be included in the GAAP measure without unreasonable efforts, and Arconic believes such reconciliations would imply a degree of precision that would be confusing or misleading to investors. In particular, reconciliations of forward-looking non-GAAP financial measures such as adjusted EBITDA and adjusted EBITDA margin to the most directly comparable GAAP measures are not available without unreasonable efforts due to the variability and complexity with respect to the charges and other components excluded from these non-GAAP measures, such as the effects of foreign currency movements, equity income, gains or losses on sales of assets, taxes and any future restructuring or impairment charges. These reconciling items are in addition to the inherent variability already included in the GAAP measures, which includes, but is not limited to, price/mix and volume.

|

Reconciliation of Combined Segment Adjusted EBITDA |

||||||||||

| (in millions) |

2008 (3) |

|

2016 | |||||||

| Net loss attributable to Arconic | $ | (941 | ) | |||||||

| Discontinued operations(1) | (121 | ) | ||||||||

| Unallocated Amounts (net of tax): | ||||||||||

| Impact of LIFO | 11 | |||||||||

| Metal price lag | (21 | ) | ||||||||

| Interest expense | 324 | |||||||||

| Corporate expense | 306 | |||||||||

| Restructuring and other charges | 114 | |||||||||

| Other(2) | 1,415 | |||||||||

| Combined segment ATOI (after-tax operating income) | $ | 532 | $ | 1,087 | ||||||

| Add combined segment: | ||||||||||

| Depreciation and amortization | 361 | 504 | ||||||||

| Income taxes | 275 | 472 | ||||||||

| Other | 6 | - | ||||||||

| Combined segment Adjusted EBITDA | $ | 1,174 | $ | 2,063 | ||||||

|

Add: Wire harness and electrical distribution adjusted EBITDA |

(115 | ) | ||||||||

|

Adjusted EBITDA including wire harness and electrical distribution |

$ |

1,059(4) |

|

|||||||

| Third party sales | $ | 14,144 | $ | 12,394 | ||||||

| Add: Wire harness and electrical distribution third party sales | $ | 1,206 | ||||||||

| Third Party Sales including wire harness and electrical distribution | $ |

15,350(4) |

|

|||||||

| Adjusted EBITDA Margin | 6.9 |

%(4) |

16.6 | % | ||||||

| Arconic’s definition of Adjusted EBITDA (Earnings before interest, taxes, depreciation, and amortization) is net margin plus an add-back for depreciation and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation and amortization. The Other line in the table above includes gains/losses on asset sales and other non-operating items. Adjusted EBITDA is a non-GAAP financial measure. Management believes that this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to Arconic’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies. |

| (1) On November 1, 2016, the former Alcoa Inc. was separated into two standalone, publicly-traded companies, Arconic and Alcoa Corporation, by means of a pro rata distribution of 80.1 percent of the outstanding common stock of Alcoa Corporation to Alcoa Inc. shareholders. Accordingly, the results of operations of Alcoa Corporation have been reflected as discontinued operations for all periods presented. |

| (2) Other includes a charge for valuation allowances related to the November 1, 2016 separation ($1,267) and a net charge for the remeasurement of certain deferred tax assets due to tax rate and tax law changes ($51). |

| (3) For 2008, a reconciliation of combined segments adjusted EBITDA to combined segments ATOI, which was the segment profit metric at the time, has been provided. A reconciliation to Net (loss) income attributable to Arconic is not available without unreasonable efforts. |

| (4) Includes the wire harness and electrical distribution business which was sold in 2009 and reflected in discontinued operations in the 2008 historical presentation. |

| 1 | Combined segment adjusted earnings before interest, taxes, depreciation and amortization (“EBITDA”) | |

| 2 | Adjusted EBITDA margins expanded from 6.9% in 2008 to 16.6% in 2016. 2008 metrics include the wire harness and electrical distribution business, which was sold in 2009 | |

| 3 | TSR calculated based on closing price from November 1st, 2016 and March 1st, 2017 | |

| 4 | Compound annual growth rate from year end 2017 to year end 2019 | |

| 5 | Adjusted combined segment EBITDA margin expansion 2016A – 2019 |

Investor Contact

Arconic

Patricia Figueroa, 212-836-2758

Patricia.Figueroa@arconic.com

or

Media Contact

Arconic

Shona Sabnis, 212-836-2626

Shona.Sabnis@arconic.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}